1. Introduction

In a global scenario, higher education has developed into an export item, thus becoming a major source of financial resources for some countries (Li et al., 2011). Depending on the source of funding, universities can be public or private (Marginson, 2011), and both compete for financial resources from private and public bodies (Carnoy et al., 2014). Universities, mainly big ones, devote a large amount of their funding to research, which yield some kind of result -publications and/or patents - (Marginson, 2007). In some universities, the appointment or continuation of a vice-chancellor and/or research di-rector may depend largely on the results obtained from academic publications indexed in the most prestigious international journals in the Journal Citation Report (JCR) or Scopus (SJR) databases (Tayyab and Boyce, 2013). The way to account for transferable products - articles and/or patents - is by means of "quality indicators" which are monitored by audits that ensure "objectivity". Quality and objectivity are two pillars that are closely linked to the language of excellence (Carpintero and Ramos, 2018); therefore, research and its results have had an effect on both researchers and universities, thus generating competition circuits.

The search for quality is not new, and the need to legitimize actions has led universities to generate evaluation, accreditation, and recognition mechanisms at both national and international levels (Bendermacher et al., 2016; Villanueva, 2011). Legitimacy is understood as a social contract (Uphoff, 1989); it favors the survival of organizations (Suchman, 1995), and plays a role of success (Dowling and Pfeffer, 1975). Therefore, the evaluation systems, among which the international ran-kings are found, legitimize the quality of the universities. Academic rankings are considered an indicator of quality and excellence that helps position universities; the best known in the international arena are Shanghai (Flórez-Parra et al., 2014; Garde et al., 2020), the Times Higher Education (THE) (Ordorika and Rodriguez, 2010), and these are closely followed by the Quacquarelli Symonds world ranking of universities, known as QS (Dobrota et al., 2016). Rankings have a methodology to define several selection criteria, there, aspects such as research on scientific publications are usually homogeneous (Gomez-Morales, 2018; Buela-Casal et al., 2007). They establish reputations because positioning can be a determining factor to attract a greater number of students (Taylor and Braddock, 2007). The United States - Anglo-Saxon culture - is the country with the highest volume of institutions in the rankings and many universities follow their guidelines (Flórez-Parra et al., 2014). However, the rankings are also viewed critically and are noted for having a governance model aligned with the neo-liberal performance-based model (Lynch, 2015). They are identified as a new form of social exclusion (Amsler and Bolsmann, 2012) and are seen as a consumer product and not as quality indicators of universities (Saunders and Blanco, 2017). They promote mercantilism and individualism (Gonzales and Núñez, 2014). In general, the countries that obtain satisfactory results in the rankings are those with the best economic capacity (Marginson, 2007). Each year, the academic rankings usually publish the lists and position of universities.

The Latin American context has been resistant to rankings, as shown by the massive student protests (Ordorika and Lloyd, 2015). There is a proliferation and elaboration of national rankings, some with a higher prestige than others, which indicates there is a comparison between universities and research centers (Escobar-Córdoba, 2009). The rankings established by countries like Colombia are a mechanism that focuses on analyzing the productivity of each university (Albornoz and Osorio, 2017). Therefore, their main function is to enhance the commoditization of higher education following a technical and operational pattern (Lynch, 2006). To do so, they take into account aspects such as training, research, level of influence in the community, and ability to strengthen ties with the productive sector through knowledge transfer (Tomàs-Folch et al., 2015).

In Colombia, there is a uniform model to verify and evaluate the quality of universities managed by the Ministry of National Education (MEN by its Spanish acronym). The academic programs offered by each university are subject to obtaining, renewing, or modifying the qualified registration, which is a mandatory and enabling requirement, and it is valid for periods of 7 years (MEN, 2019). However, universities have a greater interest to increase quality and, as a result, they certify their academic programs and the institution through prestigious organizations such as academic rankings internationally, and at a national level through the high-quality accreditation granted by the MEN (Flórez-Parra et al., 2017).

In Latin America and the Caribbean at the end of the 1990s, research was equivalent to 2.3% of the world total. Although the research lines in the accounting field are broad and diverse (Peru, Ecuador, Mexico, Colombia, Argentina, Brazil, among others), the journals positioned in the Journal Citation Reports (JCR) do not amount to more than 20 (Saavedra and Saavedra, 2015). It would be useful to analyze the research groups from the aca-demic programs of public accounting recognized by Colciencias, and to identify the publications in this field that universities subscribe to that are in the QS ranking. This could serve as a reference point to analyze the productivity of the different universities and compare the degree of influence of both public and private institutions in the national and international context.

Therefore, the objective of this study is twofold. On the one hand, based on the elements used by Colciencias, to analyze the positioning of accounting research groups in Colombian universities, and, on the other hand, to identify the volume of academic production of higher education institutions in the QS academic ranking. This analysis is relevant because research is considered a determining element to position universities both nationally and internationally.

Our study is structured as follows: the next section describes the advances and evolution of accounting research in Colombian universities; the third section explains the used methodology; the fourth section presents the results obtained, finally, the main conclusions are addressed.

2. Background of the accounting research in Colombia

The high quality of universities in Colombia is due to Law 30 of 1992 and the strong influence of the Anglo-Saxon universities led by the United States, which have adopted a more entrepreneurial and research-based management model (Flórez-Parra et al., 2019). Research in Colombian universities is established as a quality indicator since it is one of the 15 requirements for academic programs to obtain the qualified register (Higher Education Quality Assurance System, 2019; MEN, 2015), and is an essential part of the processes that guarantee the high quality accreditation of Colombian universities (MEN, 2008).

In Colombia, research is structured in two large blocks. The first one, called formative research, consists of a methodological process known as problem-based learning where students have the possibility of showing their results in congresses or scientific events. The second one, which deals with research in the strict sense, is characterized by generating knowledge that is universally recognized by the scientific community (Castaño, 2019; Gómez, 2003). Colciencias was created at the end of the 1960s as the official body to promote public policies to foster science, technology, and innovation in Colombia (MEN, 1968). One of the objectives of their national calls is to evaluate and recognize the research groups of diverse institutions such as universities. Re-search groups are classified into five categories (A1, A, B, C, and recognized) being A1 the most prestigious category; whereas researchers are classified into four levels: emeritus, senior, associate, and junior (Macias, 2016). The first call made by Colciencias took place at the beginning of the 1990s and identified 100 research groups (Villaveces, 2001). Currently, call 781 of 2017 recognizes 5,207 groups categorized as follows: A1, 523; A, 762; B, 1,168; C, 2,113; and recognized, 641. It also recognizes 13,001 researchers endorsed by universities and classified as: emeritus, 124; senior researchers, 1,707; associated researchers, 3,595; and junior researchers, 7,575 (Colciencias, 2018; 2019a). If we compare the results of call 781 in 2017 with the preliminary results published on September 6, 2019 - 833 in 2018 -, there is a slight increase in the research groups from 5,207 in 2017 to 5.727 groups in 2018. Regarding the classification of the groups endorsed by universities, a substantial improvement is observed in groups A1, A, and B (744, 977, and 1,527, respectively), and a slight decrease in the category C and recognized groups, going from 2,113 to 2,073 and from 641 to 406, respectively (Colciencias, 2019b). Therefore, the change of the university model in Colombia towards a neoliberal model of corporate and/or business and research governance is consolidating to the extent that the classification and improvement in the positioning of research groups and their researchers by both public and private universities is a reality.

The first research group recognized by Colciencias in the accounting area belonged to Universidad del Valle and achieved its category in 2004 (Patiño et al., 2021; Macias-Cardona and Cortés-Cueto, 2009). Research groups in the accounting field are concentrated in the large cities of Colombia i.e., Bogotá, Cali, and Medellín, where a greater volume of academic programs in public accounting are taught (Valero-Zapata and Patiño-Jacinto, 2012). These accounting research groups are grouped into economics and business area according to the OECD, and 457 of them are registered and recognized by Colciencias - call 781 of 2017 (Colciencias, 2019a). In 2015, 33 groups were recognized in the ac-counting field, they come from 242 public accounting programs authorized by the MEN (Patiño et al., 2016). Similar studies carried out by Patiño-Jacinto et al., (2010) identified 62 groups in 2008, Valero-Zapata and Patiño-Jacinto (2012) found 61 in the 2010 call for applications, and Macias (2016) established 62 groups recognized by Colciencias in 2016. Although there is a slight increase in the number of research groups in the public accounting academic programs, it is still incipient if we compare it with the volume of programs that operate with qualified registration, perhaps the lack of financing in research dedicated to the accounting field is one of the causes of having a smaller number of groups recognized by Colciencias.

Accounting research topics are being developed in accordance with the region's potential and the progress made by groups with research lines related to environmental accounting, social surplus accounting, government accounting, financial accounting, international financial accounting, management performance measurements, and social responsibility reporting, among others (Gómez, 2003a). The academic curricula of public accounting programs with research subjects range from 5% to 12% of the overall weight of the curricula (Patiño and Santos, 2009). The number of teachers who are part of research groups assigned to public accounting programs is 209, being 36.80% of the sample; 84 have a Ph.D., out of which only 43 have a Ph.D. relevant to the economic, administrative, and accounting sciences (Patiño-Jacinto et al., 2010).

Accounting specialized journals are scarce in Colombia and their indexation in databases such as Scopus and/or JCR are limited (Saavedra and Saavedra, 2015). The oldest journal in the accounting field in Colombia - Contaduría Universidad de Antioquia - dates to the 1980s and was published by the Universidad de Antioquia, followed by the Pontificia Universidad Javeriana - Revista de Contabilidad -, finally, Revista Lúmina of the Universidad de Manizales (Saavedra and Saavedra, 2015; Macías and Patiño, 2014). Other journals in Colombia collect academic articles on accounting such as LEGIS: Revista Colombiana de Contabilidad, Visión Contable, Apuntes Contables, Facultad de Ciencias Económicas: Investigación y Reflexión, Libre Empresa, Cuadernos de Administración, Innovar, and Activos (Rodríguez and Valdés, 2018; Mendez, 2013). Publindex is the entity in charge of assigning a positioning and classify scientific journals in Colombia. Four of them are classified as A1, A2, B and C, being A1 the most relevant quartile, and category C the least relevant (Colciencias, 2002). The two journals positioned in the accounting field - Call 830 of 2018 - are the journal of accounting university of Antioquia classified as C and notebooks of the Pontifical Javeriana University, which obtained the category B (Colciencias, 2019b). Although the journals indexed in the national databases are scarce, there were 126 accounting journals positioned in Scopus in 2015, out of which 63 are in the Q1 and Q2 quartiles, and the rest in the Q3 and Q4 quartiles. In JCR, 25 journals are identified (Macías, 2016).

3. Methodology

3.1 Sample selection

Our research focuses on Colombian institutions that operate public accounting programs on a face-to-face manner and have the character and/or denomination of university. The sample comprises 59 universities that offer 116 public accounting curricula, 21 are public and 38 are private. The universities were selected according to the National Education Information System (SNIES) data of 2019 (Figure 1).

3.2 Research methodology

3.2.1 Analysis of the information

To analyze the research groups of each university in public accounting, the first step was to identify the research groups classified by Colciencias according to call 781 of 2017 and the results published at the beginning of December 2017. To establish the research groups related to the field of study, a search was conducted using key words such as accounting, finance, tax, audit, control, and/or public management. Then, the web pages of each of the selected universities were analyzed to obtain more information about the research groups in the accounting area.

Once the groups recognized by Colciencias were determined, we proceeded to analyze the universities and the volume of academic publications registered in Scopus. This database was selected because it is one of the indicators considered by the QS ranking to classify the universities. This ranking was preferred because it is the most appropriate to analyze Latin America, and a greater number of Latin American universities are positioned in it (King et al., 2018). To identify the academic production of the universities in the Scopus database, the field of business, management, and accounting knowledge was chosen, where the greatest number of contributions from the accounting area are registered. The data from both the research groups - Sciences - and the publications made by the educational institutions - Scopus - between July and December 2019 have been consulted.

Once the data was obtained, a classification was made according to the relation of the academic public accounting programs attached to the universities (public-private) with the results obtained in the call for applications 781 carried out by Colciencias and the documents they published in Scopus. Subsequently, a cluster analysis was made, which groups the elements showing similarities to identify the public accounting research programs and groups linked to the universities, and to make a distinction and identify potential leaders in accounting research.

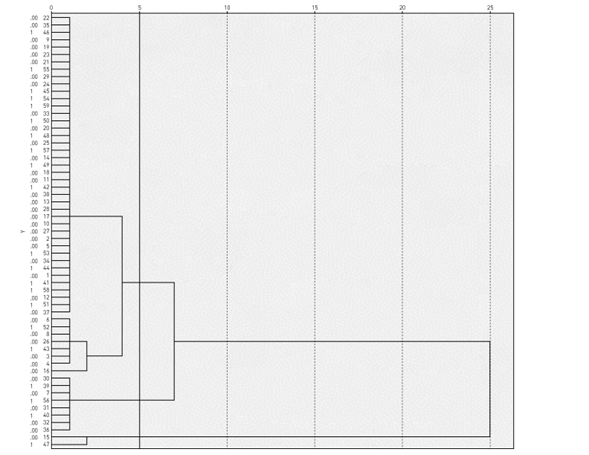

Hierarchical analysis was used to do the clustering, specifically the Ward method, and to obtain the number of groups that presented homogeneous characteristics (Ketchen and Shook, 1996). This technique was applied as seen in the dendrogram (Figure 2), three groups were formed with a distance of 5.0 points.

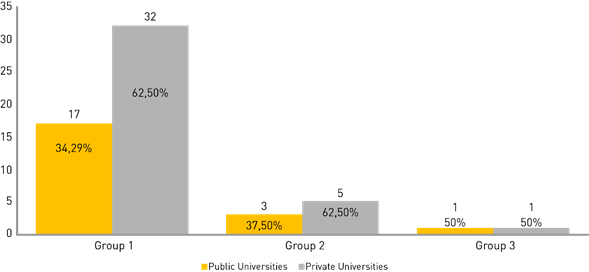

After carrying out the hierarchical analysis and identifying the clusters, we proceeded to compare the means obtained by the different groups. Therefore, the first group was composed of 49 universities, cluster two by 8, and cluster three by 2 (Figure 3). The statistical package used was SPSS version 21.0.

The first conglomerate is made up of 49 universities, where private institutions predominate (65.31%) com-pared to public ones (34.29%); in the second cluster, only 8 universities were grouped (3 public and 5 private); finally, the third cluster grouped 2 universities, 50% private and 50% public (Figure 3). In summary, we could say that there are three types of institutions: one that we could call pioneers, i.e., cluster 3; followers, cluster 2; and basic, cluster 1. Using the data taken from Colciencias, Scopus, and the clustering, we will try to analyze and identify the universities with the greatest influence in accounting research in Colombia.

Table 1 Descriptive cluster.

| N | Variables | Cluster 1 | Cluster 2 | Cluster 3 | |||

|---|---|---|---|---|---|---|---|

| N | Mean | N | Mean | N | Mean | ||

| 1. | Documents on accounting published in Scopus by university (Table 3, business, management, and accounting) | 49 | 24.88 | 8 | 172.63 | 2 | 593.00 |

| 2. | Number of recognized groups in the accounting field by university (Colciencias) (tables 1 and 2). | 49 | 1.14 | 8 | 1.00 | 2 | 2.00 |

| 3. | Total number of researchers in the accounting field by university according to creation date (Colciencias) (tables 1 and 2). | 49 | 41.63 | 8 | 36.00 | 2 | 55.50 |

| 4. | Number of researchers currently active in accounting research groups by university (Colciencias) (Web Minciencias) | 49 | 14.08 | 8 | 15.88 | 2 | 40.00 |

| 5. | Number of women researchers in accounting research groups by university (Colciencias) (Web Minciencias) | 49 | 16.14 | 8 | 12.8 | 2 | 20.09 |

| 6. | Number of men researchers in accounting research groups by university (Colciencias) (Web Minciencias) | 49 | 4.79 | 8 | 4.2 | 2 | 4.18 |

| 7. | Number of researchers recognized in call 781 of 2017 in the accounting field by university (Colciencias) (tables 1 and 2). | 49 | 3.14 | 8 | 3.75 | 2 | 9.00 |

Source: own elaboration. Based on Colciencias website (Minciencias) and tables 2, 3, and 4.

4. Discussion and analysis of results

4.1 Analysis of the results of call 781 of 2017

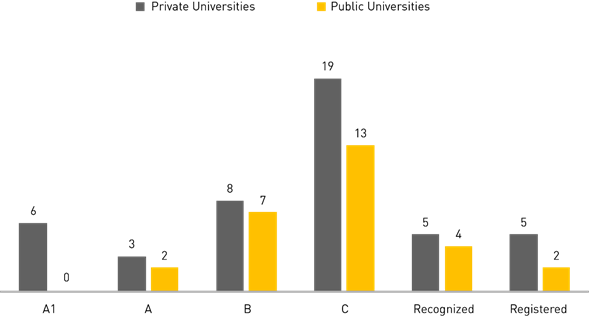

Before characterizing the clusters, we will analyze the results of the Colciencias call 781 of 2017 and the volume of publications in Scopus. First, most of the research groups belong to private universities (46), compared to public ones (28) (see tables 2 and 3). The presence of a greater number of research groups in private universities may be due to a massive privatization of the education in Colombia, since 38 out of the 59 universities that offer the public accounting program are private.

Regarding the analysis results, it is evident that the classification with the greatest presence is category C with 32 groups; followed by category B with 15 groups; recognized, 9 groups; category A1, 6 groups; finally, category A, 5 groups (see Figure 4). The measurement carried out by Colciencias highlights that most of the research groups meet around category C, which may indicate that research in the accounting field is in an embryonic stage, and that the economic resources allocated to this area of knowledge are scarce. Although in Colombia there is a will to set a minimum percentage of university budgets for research, many universities may not allocate the economic resources set for this purpose. Additionally, if we consider what Ariza and Soler (2004) have proposed regarding a series of factors such as eco-nomic recessions and salary policies implemented by companies, it is possible to state that there is a crisis in Colombian universities, which would directly affect the economic resources allocated to research.

On the other hand, Figure 4 shows that the number of groups categorized in A1 come mainly from private universities. It may seem coherent because private institutions get more resources for research than public entities, although most of the first ones have low tuition fees and few universities in Colombia offer doctorates. In the accounting field, specifically, there are no programs of this type yet. It may also be one of the causes of the doctoral professors’ shortage (Macias, 2019), who are fundamental for the advancement of accounting research (Brink et al., 2012).

Regarding category A and category B groups, the-re is a small difference between public and private universities. The first ones depend on the state budget and have a greater bureaucracy than the second ones. These aspects could be a determining factor for the presence of private university’s research groups being greater in those categories (see Figure 4).

About the recognized groups, we can say, in the first place, that some of the public universities’ research groups barely manage to obtain the minimum category in the Colciencias classification. It also happens in the private sphere (see Figure 4). Moreover, there are some universities that enjoy a reputation perhaps forged by their trajectory at an institutional level or because some of their members have occupied some relevant positions in institutions such as the Central Board of Public Accountants, the General Accounting Office, the General Attorney's Office, and the General Comptroller's Office. At present, some of these institutions are not promoting the accounting research, the approaches of the profession are more prone to the market and to be the guardians of capital. Therefore, accounting is based exclusively on the values of change protected with a series of practices and procedural norms that guarantee objectivity and legitimize activities and/or processes (Gómez, 2003b; 2006).

The results in Figure 4 also show that some research groups in public and private universities are registered but were not evaluated in call 781 of 2017. Thus, research is conducted in the institutions, which is logical because it is one of the criteria to obtain the qualified register or accreditation, the latter is of a voluntary nature. Universities must validate some minimum parameters focused on research to become endorsed institutions and to be able to compete in the educational market. Ironically, there may be universities with a qualified register or accredited institutions without research groups endorsed by Colciencias. The basic criteria requested by the Colombian Ministry of National Education may be too flexible facing the new role and approach of universities based on the paradigm of excellence and/or quality.

Tables 2 and 3 also allow us to analyze the number of researchers per university and the category assigned to them, i.e., emeritus, senior, associate, and junior. It is evident that private universities have a greater number of researchers, which guarantees better results in the Colciencias ranking. One of the ways in which universities, especially private ones, attract or recruit researchers is through economic remuneration - salaries. Stability is not a factor being considered, since in most cases the contract term in private universities is less than 12 months. In public universities, researchers are recruited through public calls; the criteria are exclusive and only the merits of the applicants are taken into account or valued. Colombian public universities should assume complementary and non-exclusive objective criteria, which could attract and/or guarantee a greater number of researchers.

4.2. Analysis of positioning in the QS ranking

The results obtained by universities in terms of the volume of documents published in the QS academic ranking in the business, management, and accounting field up to 2019 are 1,749 publications in the public sector and 2,037 in the private sector (see tables 4). Although the predominance of private universities seems evident, public universities are not immune to the change that is gradually taking place in positioning and competitiveness. The resistance of Colombian universities to a management model based on short-term results - rankings - is due to public institutions and the heterogeneity of university management models - collegial, managerial, and mixed - (Flórez-Parra et al., 2019).

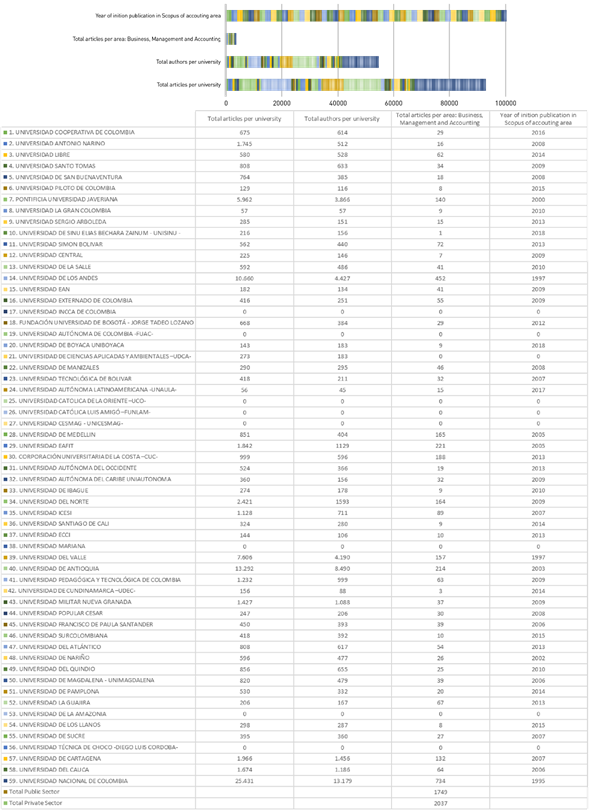

The first publications registered in the Scopus database in the Business, Management and Accounting area come from the Universidad de los Andes and date back to the 1970s with approaches to accounting from 1997. In the public sector, Universidad Nacional de Colombia published its first document in 1995. In the same way, the private universities that contribute the greatest volume of publications are, first, the Universidad de los Andes with 452 publications; followed by Universidad EAFIT with 221; Universidad de la Costa (CUC), 188; Universidad de Medellín, 165; Universidad del Norte, 164; and Pontificia Universidad Javeriana, 140. Other institutions with less than 100 publications are the Universidad ICESI, Simón Bolívar, Libre, and even the Universidad Externado de Colombia (89, 72, 62 and 55 documents, respectively). With less than 50 published documents there are Universidad of Manizales with 46 publications, both the Universidad of La Salle and the Universidad EAN with 41 documents, the Universidad Santo Tomas with 34 publications, and the Universidad Cooperativa de Colombia as well as the Universidad Jorge Tadeo Lozano with 29 contributions each (see Table 4).

The universities in the public sector that are positioned in the first places in the QS ranking are 1) Universidad Nacional de Colombia with 734 publications; 2) Universidad de Antioquia, 214 documents; 3) Universidad del Valle, 157 contributions; and 4) Universidad de Cartagena,134 published documents. With less than 100 publications, universities are ranked as follows: Universidad de la Guajira, Universidad del Cauca, Universidad Pedagógica y Tecnológica de Colombia, and Universidad del Atlántico (67, 64, 63, and 54 contributions, respectively). Other universities such as the Universidad Francisco de Paula Santander and Universidad del Magdalena reach 39 publications in the Scopus database (see Table 4).

However, the increase of publications in recent years in the university context in Colombia is largely due to the economic bonuses established in each university - public and private - and subject to the renewal of contracts, mainly in private universities, along with impact product publications - articles, books, or book chapters - by various types of research, which indicates that the rankings are distancing themselves from the faculty and becoming a product with exchange value (Gonzales and Nunez, 2014). In fact, the positioning of universities in academic rankings currently attracts a greater volume of students, which puts more pressure on universities to obtain better results in a short time and it can prevent intellectual creativity (Marginson, 2013).

Scopus databases are used by the QS ranking to position universities. One of the objective indicators is the number of citations of the published documents, which has a weight of (20%) of the index. However, the most influential academic journals are not produced by academics but by multinational corporations (Rowlinson et al., 2015). In La-tin America, only 93 universities are classified in the QS ranking: Brazil is in the first position with 22 universities; Argentina, 12 institutions; Mexico, 14 institutions; Chile and Colombia, 11 universities each; Venezuela, 5 institutions; Costa Rica, 4 entities; Peru and Ecuador, 3 universities each; Uruguay, 2 universities; finally, Puerto Rico, Cuba, and Panama with 1 university each (see Figure 5).

Table 2 Colciencias Classification of Private Universities.

| PRIVATE UNIVERSITIES | Number of Groups per University | Knowledge Area Social Sciences (Economy and Business) | Name of the Groups | Category in Call 781 of 2017 | Researchers | |||

|---|---|---|---|---|---|---|---|---|

| Emeritus | Senior | Associated | Junior | |||||

| 1. UNIVERSIDAD COOPERATIVA DE COLOMBIA | 63 | 12 | Accounting and Social Environment | B | - | - | 1 | |

| SINERGIA-UCC | C | 1 | - | 2 | ||||

| Administrative, Accounting and Economic Sciences Research Group (CACE) | B | - | 1 | - | ||||

| 2. UNIVERSIDAD ANTONIO NARINO | 37 | 4 | Accounting Office | Recognized | - | - | - | |

| 3. UNIVERSIDAD LIBRE | 95 | 15 | Harmonization and Accounting Valuation | B | - | - | 3 | |

| Accounting Management and Productivity | C | - | - | 2 | ||||

| Accounting, Economic and Administrative Trends | B | - | 1 | 3 | ||||

| Accounting Builders | A1 | - | - | - | ||||

| Accounting Alternatives | C | - | - | - | ||||

| 4. UNIVERSIDAD SANTO TOMAS | 75 | 11 | Research group in Administrative and Accounting sciences | B | - | - | 1 | |

| Research for Accounting Development INDERCON | Recognized | - | - | - | ||||

| Accounting: Information, control, and social impact | C | - | - | 1 | ||||

| 5. UNIVERSIDAD DE SAN BUENAVENTURA | 71 | 5 | Organizational Management and Human Development | B | - | - | 2 | |

| 6. UNIVERSIDAD PILOTO DE COLOMBIA | 9 | 3 | Innovation and Competitiveness in Organizations (ICO) | C | - | - | 3 | |

| 7. PONTIFICIA UNIVERSIDAD JAVERIANA | 123 | 8 | Accounting Integration and Context | C | - | - | 2 | |

| 8. UNIVERSIDAD LA GRAN COLOMBIA | 27 | 8 | Accounting, Financial and Tax Management. | C | - | - | 1 | |

| Contemporary Accounting Trends: Control, Management and Governance | C | - | - | 1 | ||||

| Interdisciplinary Studies in Accounting | C | - | - | - | ||||

| 9. UNIVERSIDAD SERGIO ARBOLEDA | 22 | 3 | - | - | ||||

| 10. UNIVERSIDAD DE SINU ELIAS BECHARA ZAINUM - UNISINU - | 19 | 2 | FACEAC Accounting and Administration | C | - | - | 1 | |

| 11. UNIVERSIDAD MARIANA | 18 | 3 | Accounting Identity | B | 3 | |||

| 12. UNIVERSIDAD SIMON BOLIVAR | 31 | 2 | Accounting Thought and International Management | A | - | - | 4 | |

| 13. UNIVERSIDAD CENTRAL | 17 | 3 | ATARALAWAA AMAA | Recognized | - | - | - | |

| 14. UNIVERSIDAD DE LA SALLE | 41 | 7 | Responsibility, Accountability and Transparency | Recognized | - | - | 1 | |

| 15. UNIVERSIDAD DE LOS ANDES | 155 | 10 | Studies in finance and financial economics | A1 | - | 2 | 1 | |

| 16. UNIVERSIDAD EAN | 13 | 5 | G3PyMES: Management group in large, small, and medium-sized companies | A1 | - | 1 | 4 | |

| 17. UNIVERSIDAD ECCI | 11 | 1 | Research Group in Economic and Administrative Sciences -GICEA- | B | - | - | - | |

| 18. UNIVERSIDAD EXTERNADO DE COLOMBIA | 35 | 4 | Information Systems and Organizational Control - SICO. | Registered | ||||

| 19. UNIVERSIDAD INCCA DE COLOMBIA | 10 | - | - | - | ||||

| 20. FUNDACIÓN UNIVERSIDAD DE BOGOTÁ - JORGE TADEO LOZANO | 29 | 7 | Study Group on Accounting Information and Control. | C | - | - | - | |

| 21. UNIVERSIDAD AUTÓNOMA DE COLOMBIA -FUAC- | 23 | 3 | Accounting Universe | C | - | - | - | |

| 22. UNIVERSIDAD DE BOYACA UNIBOYACA | 16 | - | GISEDE Business Sector Research and Economic Development Research Group | Registered | ||||

| 23. UNIVERSIDAD DE CIENCIAS APLICADAS Y AMBIENTALES -UDCA- | 12 | - | Compensation With Social Justice | Registered | ||||

| 24. UNIVERSIDAD DE MANIZALES | 16 | 4 | Accounting Theory | Recognized | - | - | 1 | |

| 25. UNIVERSIDAD TECNOLÓGICA DE BOLIVAR | 18 | 1 | - | - | ||||

| 26. UNIVERSIDAD AUTÓNOMA LATINOAMERICANA -UNAULA- | 10 | 1 | GICOR Accounting and Organizations Research Group | C | - | - | 1 | |

| 27. UNIVERSIDAD CATÓLICA DE ORIENTE -UCO- | 17 | 1 | FACEA | C | - | - | 1 | |

| 28. UNIVERSIDAD CATÓLICA LUIS AMIGÓ -FUNLAM- | 13 | 3 | CONTAS - Environment and Society Accounting | C | - | - | 2 | |

| 29. UNIVERSIDAD CESMAG - UNICESMAG- | 14 | 2 | LUCA PACCIOLI | C | - | - | - | |

| SYNERGY | Registered | |||||||

| 30. UNIVERSIDAD DE MEDELLIN | 31 | 9 | Accounting Research and Public Management Group | C | - | - | - | |

| 31. UNIVERSIDAD EAFIT | 43 | 7 | Information and Management | A | - | - | 2 | |

| 32. CORPORACIÓN UNIVERSITARIA DE LA COSTA -CUC- | 22 | 3 | Research Group in Accounting, Administration and Economics - GICADE | A | - | 2 | 3 | |

| 33. UNIVERSIDAD AUTÓNOMA DEL OCCIDENTE | 24 | 4 | Grupo de Investigación en Contabilidad y Finanzas-GICOF | C | - | - | - | |

| 34. UNIVERSIDAD AUTÓNOMA DEL CARIBE UNIAUTONOMA | 27 | 3 | ERCONFI: Education and Technology, Economy and Region, Public Accounting, Business, Finance, and related. | A1 | - | 1 | 2 | |

| 35. UNIVERSIDAD DE IBAGUE | 9 | - | UNIDERE Research Group | Registered | ||||

| 36. UNIVERSIDAD DEL NORTE | 18 | 3 | Innovate in the Caribbean | A1 | - | 2 | 3 | |

| 37. UNIVERSIDAD ICESI | 14 | 4 | Investment, financing, and control | A1 | - | 1 | 1 | |

| 38. UNIVERSIDAD SANTIAGO DE CALI | 21 | - | GICONFEC Accounting, Financial and Economic Research Group | C | - | - | 1 | |

| Total | 46 | 1 | 12 | 55 |

Source: Own elaboration. Based on Colciencias data (781-2017).

Table 3 Colciencias classification of Public universities.

| PUBLIC UNIVERSITIES | Number of Groups per University | Knowledge Area Social Sciences (Economy and Business) | Name of the groups | Category in Call 781 of 2017 | Researchers | |||

|---|---|---|---|---|---|---|---|---|

| Emeritus | Senior | Associated | Junior | |||||

| 39. UNIVERSIDAD DEL VALLE | 173 | 12 | Contemporary Topics in Accounting, Control, Management and Finance | C | - | - | - | - |

| 40. UNIVERSIDAD DE ANTIOQUIA | 272 | 10 | Accounting Research and Consulting Group - GICCO - UDEA- | C | - | - | 1 | 1 |

| Accounting Dynamics Group -GIDICON- | C | - | - | - | 1 | |||

| History, Education, Economy, Accounting and Society: HECOS | C | - | - | - | 2 | |||

| 42. UNIVERSIDAD DE CUNDINAMARCA -UDEC- | 24 | 3 | DOPYS, Organizational, prospective, and sustainable development | C | - | - | 1 | 2 |

| 43. UNIVERSIDAD MILITAR NUEVA GRANADA | 64 | 4 | Group of Contemporary Studies in Accounting, Management and Organizations - GECCGO | B | - | - | 2 | 2 |

| GECS (Group of Studies in Education, Accounting and Society) | Recognized | - | - | - | 1 | |||

| 44. UNIVERSIDAD POPULAR CESAR | 39 | 3 | Infinite apollo | B | - | - | - | 5 |

| 45. UNIVERSIDAD FRANCISCO DE PAULA SANTANDER | 50 | 10 | CINERA Accounting Research Group | C | - | - | - | 1 |

| 46. UNIVERSIDAD SURCOLOMBIANA | 42 | 3 | - | - | - | - | - | - |

| 47. UNIVERSIDAD NACIONAL DE COLOMBIA | 585 | 25 | Accounting, Organizations and Environment | B | - | 1 | 1 | - |

| Accounting Observatory | C | - | - | - | 1 | |||

| Interdisciplinary studies on management and accounting (INTERGES) | A | - | 1 | 4 | 4 | |||

| 48. UNIVERSIDAD DEL QUINDIO | 53 | 4 | Research Group in International Comparative Accounting | Recognized | - | - | - | 1 |

| 49. UNIVERSIDAD DE MAGDALENA - UNIMAGDALENA | 49 | 4 | Research group in Accounting, Finance and Auditing: CONFIA | Registered | - | - | - | - |

| 50. UNIVERSIDAD DE PAMPLONA | 51 | 3 | CE and CON Business and Accounting Sciences Research Group | C | - | - | 1 | 1 |

| 51. UNIVERSIDAD DE LA GUAJIRA | 53 | 12 | GECAES. Accounting, Administrative, Economic and Social Management. Interdisciplinary group of Socio-Economic, Accounting, Administrative, Technological, Innovation, ICTs, and Public Policies management. | A | - | 1 | 1 | 1 |

| Research in Budget Accounting and Finance - ICOPREFI- | C | - | - | - | - | |||

| 52. UNIVERSIDAD DE LA AMAZONIA | 29 | 3 | CIFRA - UMBER - Collective of Financial Research in the Amazon Region- | C | - | - | - | 1 |

| Amazon footprint | C | - | - | - | 3 | |||

| SINAPSIS | B | - | - | 1 | 3 | |||

| 53. UNIVERSIDAD DE LOS LLANOS | 32 | 6 | GYDO Organizational Management and Development | C | - | - | - | - |

| 54. UNIVERSIDAD DE SUCRE | 26 | 3 | Research Group on Production Management and Organizational Quality | C | - | 1 | - | 1 |

| 55. UNIVERSIDAD TÉCNICA DE CHOCO -DIEGO LUIS CORDOBA- | 16 | - | Accounting Innovation | Recognized | - | - | - | - |

| 56. UNIVERSIDAD DE CARTAGENA | 94 | 7 | GIDEA Environmental Studies Research Group | Recognized | - | - | - | - |

| 57. UNIVERSIDAD DE NARIÑO | 55 | 3 | REPCONTA | Registered | ||||

| 58. UNIVERSIDAD DEL CAUCA | 65 | 7 | Accounting, Economic and Administrative Research -GICEA- | B | - | - | - | - |

| Accounting, Society and Development | B | - | - | 1 | - | |||

| 59. UNIVERSIDAD DEL ATLÁNTICO | 82 | 3 | Sustainable Organizations | B | - | 1 | 1 | 5 |

| Total | 28 | 0 | 5 | 14 | 36 |

Source: Own elaboration. Based on Colciencias data (781-2017).

Table 4 Documents published in Scopus by private and public universities.

Source: Own elaboration. Based on Scopus 2019.

In Colombia, only 11 universities are positioned in the QS ranking, 4 public sector and 7 private. The best universities, at the top of the QS ranking are Universidad de los Andes, ranked 272; Universidad Nacional de Colombia, ranked 275; and Universidad Externado de Colombia, ranked 407 (see Table 5). Since universities depend on a volume of citations in the databases - Scopus -, the low visibility of Colombian universities may be partly due to what Marginson (2007) states: documents published in languages other than English are less published and less cited.

Source: Own elaboration. Based on the QS ranking.

Figure 5 Universities positioned in the QS ranking 2019.

Table 5 Colombian Universities the QS ranking 2019.

| Colombian Universities | Position | Character |

|---|---|---|

| Universidad de los Andes | 272 | Private |

| Universidad Nacional de Colombia | 275 | Public |

| Universidad Externado de Colombia | 407 | Private |

| Pontificia Universidad Javeriana | 521-530 | Private |

| Universidad de Antioquia | 701-750 | Public |

| Universidad de la Sabana | 801-1000 | Private |

| Universidad del Norte | 801-1000 | Private |

| Universidad del Rosario | 801-1000 | Private |

| Universidad del Valle | 801-1000 | Public |

| EAFIT University | 801-1000 | Private |

| Universidad Industrial de Santander - UIS | 801-1000 | Public |

Source: Own elaboration. Based on the QS ranking.

Although Table 5 shows that Colombian universities manage to obtain a representative number in the QS ranking, their influence in the region is scarce. This may indicate that the research in Colombian universities is not having a significant impact although there are some exceptions, e.g., Universidad de los Andes and Uni-versidad Nacional de Colombia, which are positioned within the top 300 of the QS ranking. However, the results are framed by university and not by the contributions of the public accounting academic programs.

4.3. Cluster Analysis

Finally, we will perform the cluster analysis (Table 1). Cluster 3 is composed by two universities (public and private). The first one has a higher volume of publications in the accounting field than the second one, these results coincide partially with the ones disclosed by the QS ranking. Furthermore, it is relevant that only two universities lead and concentrate a greater number of publications in the Scopus database than the other groups, which are integrated by a greater number of universities (see Figure 6)1. Although there are still few universities positioned in the rankings, it is worrying that public institutions are joining the market-based university management model. This approach could be due to the regulatory frameworks established in Colombia.

Cluster 2 universities are mostly in the private sector. The cluster shows an interest in publications and is po-sitioned in the second place if we compare it with cluster 3. In relation to the number of active researchers and the number of researchers recognized by Colciencias, its scores are higher than those obtained by Cluster 1. This is logical to the extent that private universities depend mainly on sources of funding, enrolment, and private capital investments, which generates more competitive institutions and yield short-term results. Therefore, they are directly related to the management model, as they seek indicators of quality and excellence to attract a greater number of students and researchers.

Likewise, Cluster 1 is characterized by the high number of universities (49) and by the predominance of private universities. This group presents some results that show the high rotation of researchers. On the one hand, the scores related to researchers that create the groups in Colciencias are high (41.63), contrary to the number of researchers that the universities currently have (14.08). This finding shows that some universities hire researchers for a specific period of time; those hiring times coincide with the renewal or application for accreditation and/or qualified register by the institutions. Therefore, they focus more on teaching than on research. On the other hand, this is the only cluster that obtains a higher value in attracting male researchers, although in the variable documents published in Scopus, it does not obtain the best results. This may be a result of a structural exclusion that makes the processes that are not captured by the measurement models invisible, which generates a passive and unconscious resistance towards the rankings.

5. Conclusions

The change in the management model at universities and the strong influence of the Anglo-Saxon sphere in Colombia is evident, and the public accounting programs have not been unaware of these changes, to the extent that universities are increasingly focused and positioned on the criteria to measure research and quality, i.e., rankings. Quality based on international rankings gene-rates great inequalities and favors universities with large economic resources, thus generating new priorities that benefit universities that are geographically located in developed countries. Therefore, Latin American uni-versities, especially Colombian ones, must focus their efforts on building a university management model in accordance with the needs of the territory, considering aspects such as identity, administrative culture, or the ability to strengthen public sector universities with greater funding.

Research in the accounting field in Colombia is supported by minimum parameters regulated by the Ministry of National Education, i.e., qualified register, high quality accreditation and/or Colciencias. The processes to classify research groups together with the paradigm of high quality universities guarantee a homogenization in the educational system. However, at the same time, they take away and anesthetize the universities’ social mission by making them focus on the market. In addition, the measurement systems could be generating, in turn, a new type of researchers, some very oriented to write papers (articles), and others very interested in meeting the minimum criteria (emeritus, senior, associate, and junior) established by the entities that regulate the positioning of research in Colombia. In this way, if universities and researchers have been assuming this new market-oriented role, the universities may be losing the critical, reflective, and paused character that has characterized them.

It is evident that accounting research in Colombian universities is at an embryonic phase, maybe because it has not been given the relevance and/or support it requires by the different institutions. The lack of a complete diagnosis and greater traceability of the current state of research in Colombia poses significant questions about the system that regulates and establishes indicators and metrics such as Minciencias (Gómez, 2022). Although the results may have improved compared to the number of research groups recognized by Colciencias’ previous calls, most of the research groups fall into a basic category (C), which is worrying for the progress of research in the accounting field. The question is whether the proliferation of academic programs with qualified records, together with the virtualization of the public accounting career in Colombia, may be generating, on the one hand, a greater commodification of the profession and this in turn be seen more as an accounting technique and not as a science that analyzes and studies the phenomena and social relations of production and distribution of its environment (Rojas-Rojas et al., 2021; Arévalo and Quinche, 2008). Therefore, universities may be in a crisis linked to three characteristics currently accentuated in the university sphere: hegemony, legitimacy, and institutionality; the latter is very much associated with the financial crisis, which generates large cuts in the public sector (De Sousa, 2010).

Minciencias’ metrics to classify groups and researchers through different calls with changing evaluation criteria generates, on the one hand, an unstable horizon for the projection of research programs in the accounting field. On the other hand, there is not a response time in accordance with the efforts made and demanded by the research processes. Furthermore, the lack of transparency and more efficient access to the information provided by the Higher Education System (SES by its Spanish acronym) and the Science and Technology System (SCYT by its Spanish acronym) makes it very difficult to compare, track, consolidate, and verify information.

One of the limitations of this document is that it is based on Minciencias measurement systems and on the 2017 call, prior to the last one. This would lead to differences in the analysis of the measurement model established by Minciencias.

This study can contribute to the literature, particularly to analyze the progress and/or state of research in the various academic programs and the impact and influence obtained in academic rankings. This could serve as a starting point to compare the environment at universities and countries, thus allowing a more in-depth study of the phenomenon and a comparison of results with other countries.